Building a strong personal finance emergency fund is one of the most important steps toward financial security. Life is unpredictable, and unexpected expenses can come at the worst time. Whether it is sudden job loss, medical bills, car repairs, or urgent home needs, having the right savings target, organized sinking funds, thoughtful budgeting, and storing money in a high yield account can protect you from stress and debt. Instead of worrying when emergencies strike, you gain confidence knowing you are prepared.

Many people delay building a personal finance emergency fund because they feel overwhelmed or believe they do not earn enough to save. But even small, consistent effort makes a powerful difference. Planning, discipline, and awareness can gradually build a financial safety net that supports you during difficult moments. When your finances are protected, your peace of mind improves too.

Why You Need A Personal Finance Emergency Fund

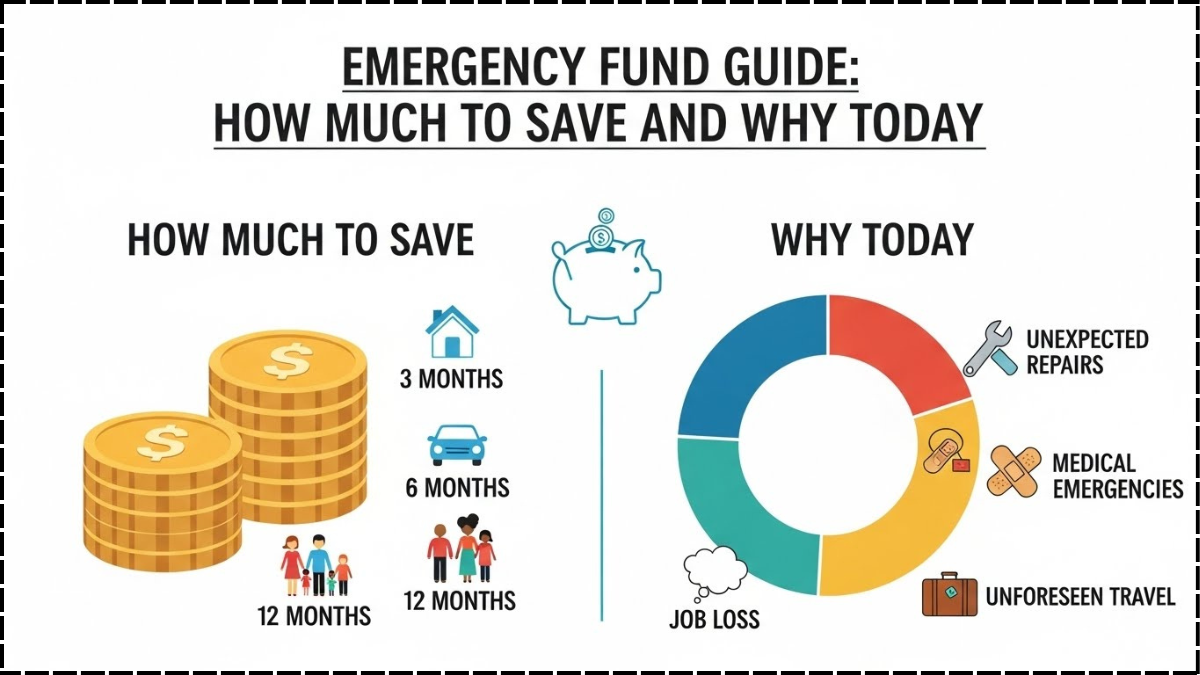

A personal finance emergency fund acts as a financial shield. Without it, people often turn to loans, credit cards, or borrowing from friends, which leads to debt and stress. Setting a realistic savings target helps create structure instead of guesswork. Experts often suggest building three to six months of living expenses, but even one month of savings is an excellent start.

Along with emergency funds, structured sinking funds allow you to plan for predictable but irregular expenses such as yearly insurance, school fees, or maintenance costs. This reduces financial shock because these expenses no longer feel unexpected. When combined with disciplined budgeting, your money becomes organized, controlled, and more purposeful. Finally, saving this money in a high yield account ensures your emergency fund grows securely while staying easily accessible.

Table: Key Elements Of A Strong Emergency Fund

| Element | Purpose | Benefit |

|---|---|---|

| personal finance emergency fund | Protection from unexpected expenses | Reduces stress |

| savings target | Decides how much to save | Clear financial direction |

| sinking funds | Plans non-monthly costs | Prevents budget shock |

| budgeting | Organizes income and spending | Improves control |

| high yield account | Stores emergency savings | Earns better interest |

How To Build Your Savings Target Step By Step

A successful personal finance emergency fund starts with a savings target that suits your lifestyle. Begin by calculating essential monthly expenses such as rent, bills, groceries, transportation, and medical needs. Multiply that by the months you want covered. This becomes your emergency goal. Some people may only manage small contributions at first, and that is perfectly fine. Consistency matters more than speed.

Once your savings target is defined, combine your strategy with sinking funds to handle planned irregular costs. This keeps your emergency savings untouched for real emergencies only. Smart budgeting is the engine behind this system. Allocate a portion of income each month toward savings before spending on other things. Finally, keep your emergency savings in a high yield account so that it grows while staying accessible when truly needed.

Making Emergency Funds Easier And More Practical

The journey of building a personal finance emergency fund becomes easier when broken into manageable habits. Automating transfers helps maintain consistency so saving doesn’t rely on memory or motivation. Reviewing your budgeting monthly allows you to adjust contributions and stay on track. Expanding sinking funds gradually strengthens your financial structure, reducing the chance of dipping into emergency money unnecessarily.

Storing your savings in a high yield account keeps funds separate from spending accounts, reducing temptation. Over time, seeing your fund grow builds confidence and financial independence. Even slow progress creates meaningful security. With patience and discipline, your emergency savings transform from a fearful challenge into a powerful financial advantage.

Bullet Highlights To Remember

- Build a personal finance emergency fund for financial safety

- Set a realistic savings target based on living expenses

- Use sinking funds for planned irregular costs

- Practice disciplined budgeting to support saving

- Keep money in a secure high yield account for growth and access

Conclusion

Financial peace does not come by luck; it comes through planning. A well-built personal finance emergency fund supported by a clear savings target, thoughtful sinking funds, disciplined budgeting, and a reliable high yield account gives you control during uncertain times. This financial cushion protects you from debt, reduces anxiety, and builds confidence. No matter where you are starting, every step toward saving strengthens your future. With patience and consistency, you create a financial foundation strong enough to handle whatever life brings.

FAQs

What is a personal finance emergency fund?

A personal finance emergency fund is money saved specifically for unexpected expenses like job loss, medical emergencies, or urgent repairs.

How much should my savings target be?

Your savings target is often three to six months of essential living costs, although starting with a smaller goal is also helpful.

Why do I need sinking funds?

Sinking funds help plan predictable but irregular expenses so they don’t disrupt your emergency savings.

How does budgeting help?

Budgeting organizes income and spending, making it easier to consistently contribute to your emergency and sinking funds.

Why use a high yield account?

A high yield account keeps your emergency savings safe while earning better interest and staying accessible when needed.

Click here to learn more